Stop skating to where the puck is

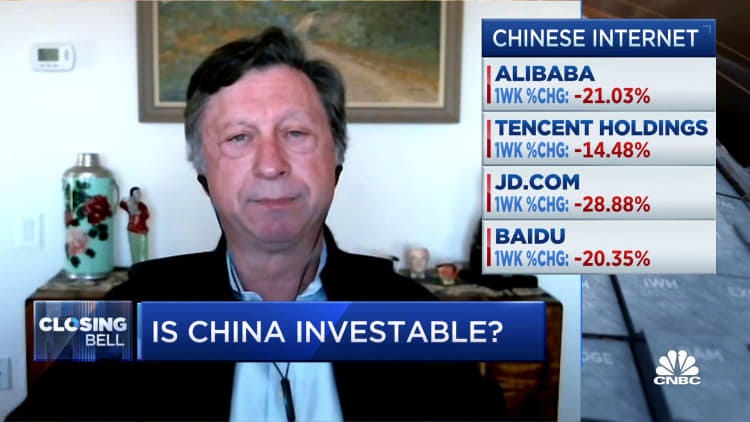

About thrice a week I come across the latest trending explainer about how the growth vs. profitability paradigm has shifted in public and private markets. Every board meeting features a long discourse about how “the macro environment has shifted” which means that every tech company needs to be profitable, like yesterday, regardless of whether its runway is 3 months or 3 years.

I just have one question for these macro valuation obsessives…. do you ever get tired of skating only to where the puck is?

I skate to where the puck is going to be, not where it has been. - Wayne Gretzky

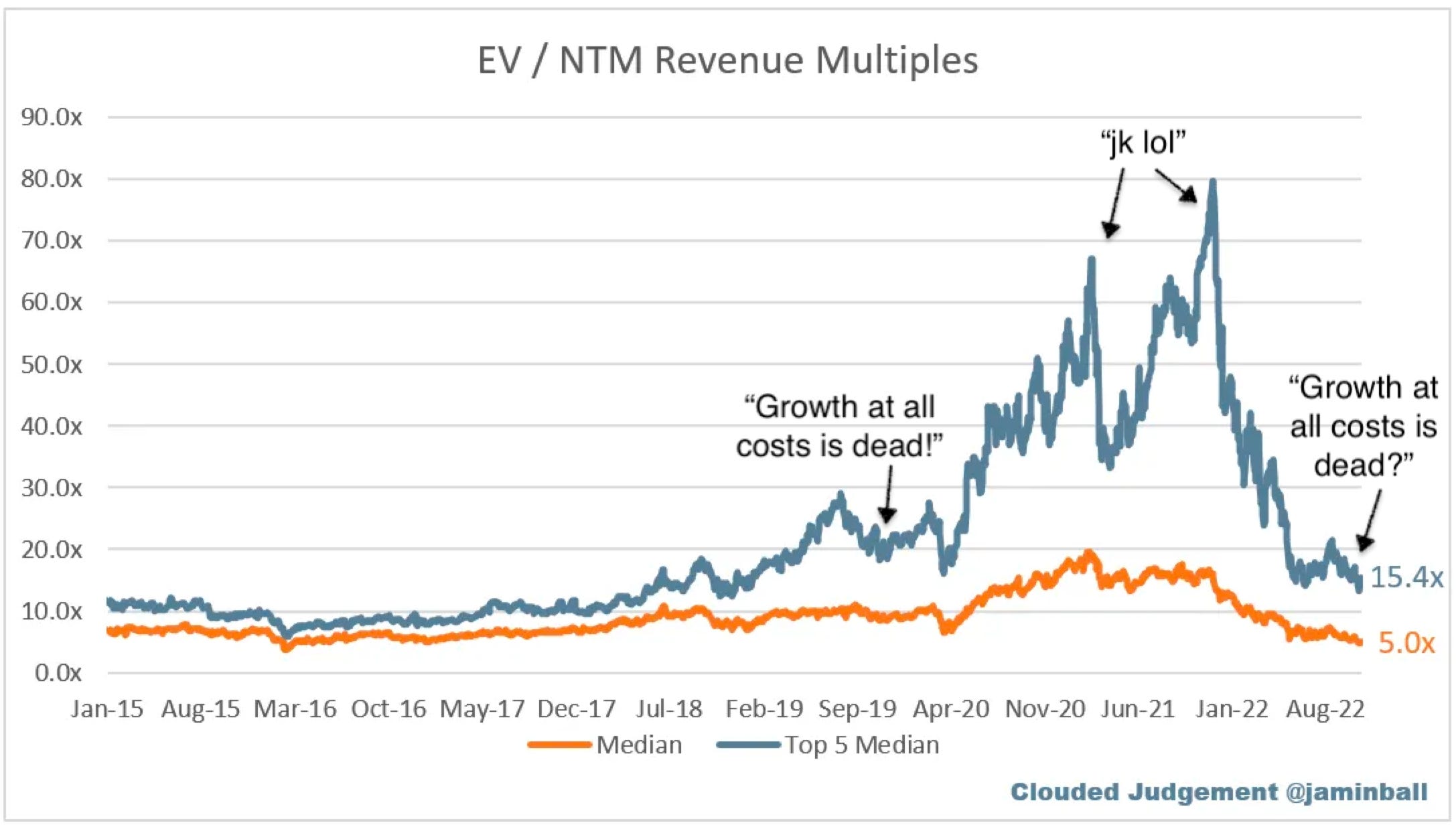

I am old enough to remember a time before the coronavirus, way way back in the ancient time period of fall 2019, when a little-known company called WeWork failed to go public in such a dramatic fashion that the entire technology sector went into an absolute frenzy about how “growth at all costs” was dead forever. Remember what happened next?

Growth tech companies of all sizes have been engaged (along with their boards) in a dizzying see-saw over the past couple of years…

Spring 2019 (when Uber went public): Grow, grow, grow! And sell your shares to the public before people start worrying about unit economics.

Fall 2019 (when WeWork tried to go public): Growth is out, profitable growth is in!

Spring 2020 (covid-19): The world is literally ending. “Furlough” becomes one of Webster’s words of the year.

Fall 2020-Fall 2021: Stocks are rising and we don’t know why. Not only do net margins not matter anymore, but gross margins don’t, either. Number go up. Peloton is the AWS for fitness?

2022: RIP Growth at all Costs. Sixteen thousand second-year VC associates launch their Substacks with an inaugural “how to survive in a downturn” post. (oh, the irony)

If I were a founder, this endless cascade of shifting expectations would probably tick me off. Not because I wouldn’t appreciate the reality check (“markets can stay irrational longer than you can stay…”) but because the paired advice comes with two enormous problems: One, it’s based on the notion that the current environment will stay the way it is forever; and Two, it fails to acknowledge that all prior advice was also based on the idea of macro conditions never changing, and was therefore spectacularly wrong when the winds did indeed shift.

So when you see those funny tweets saying something like “Lord please give me the confidence of a VC who was telling me last November that I should 4x my burn” just note the possibility(!!) that current advice to cut to profitability immediately might(!!!!!) end up looking just as goofy in retrospect.

And while the advice to spend conservatively may end up being right… could we have a little humility please? And maybe some situational awareness. Does the company need to fundraise in the next 6 months? Well, yeah, the best information we have available suggests that investors are going to demand a credible path to profitability in a pretty narrow timeline. But what if the company raised a bajillion dollars last year and still has most of it left? And has a great product, is super sticky, good NRR, et cetera? Why does that company need to be concerned with today’s very short term investor preferences?

And furthermore, what if the financing market shifts back into growth mode 2 years from now, and you spent your entire last two years focused on anything but growth? I’m not saying this is definitely going to happen, but why are you so convinced that it has no possibility of happening?

It’s strange to me that while it’s now clear that during last year’s euphoria we should have been saying “the market might be over-prioritizing growth, so let’s rotate somewhat towards efficiency to be better prepared for when the market inevitably shifts”, today I never hear anyone say “the market seems to have fiercely overcorrected towards profitability and away from growth, I think that growth might be temporarily undervalued which means let’s not dismiss it." Huh.

Investing, and company-building, both demand that we make educated guesses about where the puck might be, and work assiduously to make decisions that optimize for that range of possible futures (possible puck locations). Yet we have a very human tendency to extrapolate our current conditions out forever, to allow price to drive narrative. And this is tough to overcome, it seems hardwired to a degree.

It doesn’t help that we live in the midst of The Vortex of the Long Now (also known as Twitter), with an absolutely endless deluge of chatter and analysis of what just happened and why it’s bad. It’s hard to get away from. And it’s true that Only The Paranoid Survive. But as stewards of capital and of businesses, when the little voice in our head tells us to freak the f— out about the macro climate, it behooves us to at least consider a version of the world where things aren’t bleak and grim forever. How can we chastise the 2021 versions of ourselves for not considering the possibility of changing conditions, yet not consider the very same thing about what we say and believe in 2022?

We can’t predict the future with any kind of fidelity, but we can at least have the courage to use our imaginations to try.