What caused the 2020 SaaS bubble and why is it now popping?

Pain. Pain and the color red. That’s what I see when I look at my portfolio these past few months. Not only is the S&P kicking my ass, but the NASDAQ 100 is too — specifically because I’m allocated heaviest in the mid-cap SaaS sector, where multiples have dropped precipitously since November. If you’re reading this there’s a pretty good chance you’re in the same boat.

In order to understand what’s happening, we first have to grasp how we got here in the first place. Why did SaaS valuations — which spent 2018 through 2020 at elevated but perhaps not excessive multiples — rocket into bubble territory just a few months after the start of the lockdowns?

My mental model has 3 main drivers, all of which have to do with how valuations are estimated in discounted cash flow (DCF) models. DCF models — particularly for SaaS businesses — are highly sensitive to three main variables: 1) The rate of growth persistence; 2) discount rates; 3) how earnings are calculated.

1. Growth persistence

Growth persistence is a measure of how quickly growth decays in a business. Hypergrowth businesses cannot stay in hypergrowth forever, otherwise Amazon would be growing at 600% annually even as revenues surpass $400 billion — growth on a percentage basis tends to decrease with scale. If a company grows 50% in one year and then 40% the following year, their measured growth persistence is 80% (.40/.50).

Several smart statistics-minded VCs have determined that growth persistence rates average in the low-to-mid 80’s over large sample sizes. You can build your DCF model with 85% as the input and get revenue build assumptions like below:

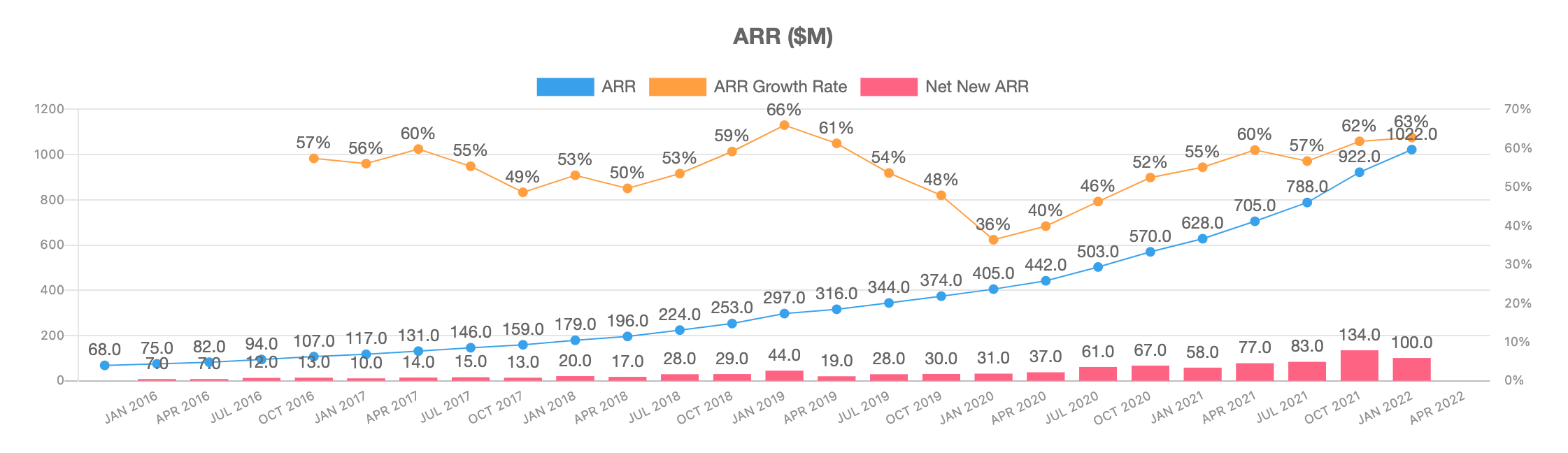

But a funny thing happened in 2020 and 2021 — growth persistence rates for many public SaaS companies rocketed above 100%, meaning that many of these companies were growing ARR faster than in the prior 12 month period.

For example, here’s DocuSign:

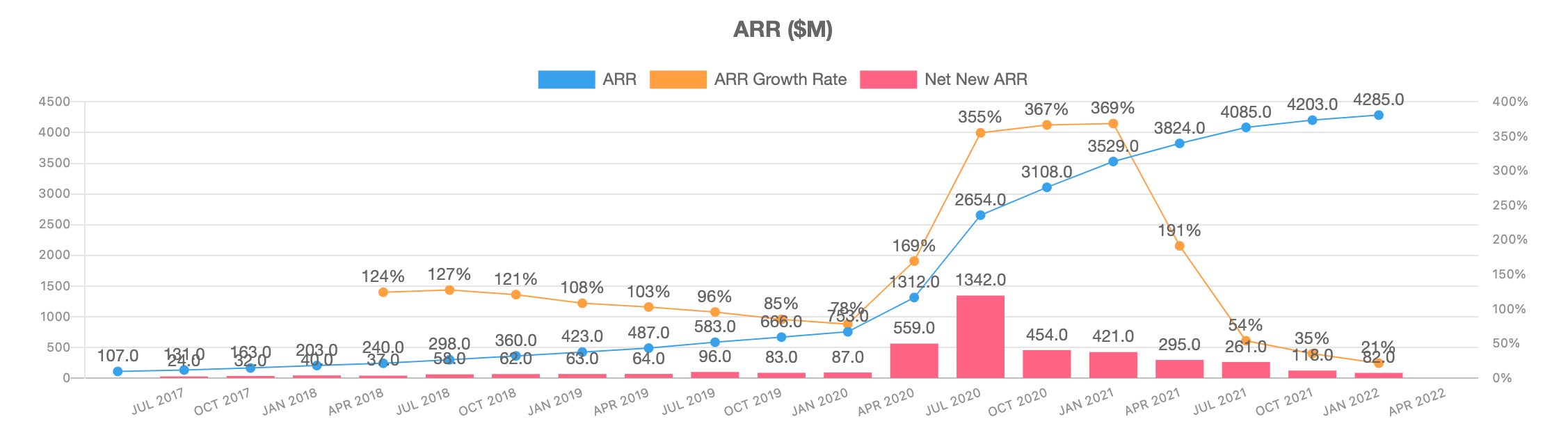

ZScaler:

And the canonical example, Zoom:

(By the way, these charts are from PublicComps — you should check them out if you’re interested in this stuff. I have no relationship besides being a customer who occasionally shares product feedback with the co-founders.)

There are many good reasons for this: Lockdowns accelerated the adoption of digital infrastructure (especially collaboration/communications), and government and central bank actions flooded the economy with capital that had to be spent somewhere.

One thing we didn’t know at the time was whether this growth was a one-time “pull-forward” or whether this level of acceleration was “the new normal”. Even if you wanted to conservatively predict that it was mostly a “pull-forward”, you could still talk yourself into the idea of big time macro tailwinds coming up ahead from “the Great Reopening”.

The trouble is that even if you are attempting to be conservative, small differences in growth persistence lead to absolutely massive differences in valuations as determined by DCF models. For example, look at what happens when you compare a 80% growth persistence input with a 90% one in this DCF:

That’s a more than 3x difference in valuation — whoa!

The analyst using the 80% figure likely did it in a time period when average growth persistence rates were in the mid-80s, “to be conservative”. What’s a conservative estimate in a year when all the stocks you’re tracking had 110-130% rates of growth persistence? “Maybe 90%, to be conservative”? See the problem here?

2. Discount rates

Valuations are incredibly sensitive to discount rates. This is something you can sense from seeing how the market reacts to very small adjustments to rates by the Federal Reserve, but you can really feel it for yourself once you get inside the DCF model and see how higher rates can collapse valuations.

We take the discount rate in this DCF from 12% to 20% and the valuation collapses by nearly 2/3s.

This of course is what happened to interest rates in mid-2020:

(source)

(source)

The discount rates used in valuations are closely tied to interest rates, but are also sector-specific — how easy is it for investors to obtain capital (have you seen how much money the big crossover funds raised in the past two years?). Or, more subjectively: How uncertain is the future of this particular sector of the economy? Less perceived uncertainty means lower discount rates, regardless of how certain or uncertain the future actually is.

You may remember that as the 2010s chugged along there was an increasing sense that the SaaS business model had been “figured out”. The decade’s accumulated artifacts of this wisdom included the works of Jason Lemkin, the Predictable Revenue playbook, David Skok’s SaaS metrics compendium, the Bessemer Cloud Index, and so on. SaaS was no longer the frontier of mavericks and renegades, it became institutionalized, with a codified playbook and standardized metrics.

Because SaaS businesses have recurring revenues (which means you can count on them… well, recurring), a well-understood business model, and a vast supporting network of 3rd party tools to handle hosting/billing/payments/accounting/whatever, these companies have lower uncertainty and lower risk. Nobody would seriously argue that starting a SaaS company is harder in 2021 than in 2011. With less risk means many new entrants which means a lower expected level of required return — and therefore, once again, lower discount rates.

So far we have the bubble being fueled by 1. higher projected rates of growth persistence (dramatically increasing estimated terminal values of businesses) and 2. lower discount rates (same). The third and last big effect was…

3. How earnings are calculated for the purposes of valuation (or: How I Learned to Stop Worrying and Love Stock-Based Compensation)

There’s a saying that once a measure becomes broadly known, it starts to be less meaningful because it can be gamed. This is precisely what happened to “Free Cash Flow” (and its cousin, “Adjusted EBITDA”) and explains why hardly any public SaaS growth companies are GAAP profitable.

In The Decade The World Discovered SaaS Was Awesome (i.e. the 2010s), an interesting fact propagated about these businesses: While many of the SaaS hypergrowers continued to post negative earnings even at ARR run rates above $500m, many of them did have positive free cash flows because these businesses often involve a lot of customers pre-paying for their annual subscriptions. Put another way, SaaS companies often have tremendously strong cash conversion cycles.

Now, having strong cash conversion is certainly a great advantage for a business and one of the reasons why SaaS is great (not a SaaS company, for the most part, but Amazon is famous for taking advantage of this capability). But here’s the thing: Saying that a company has significantly larger cash flows than their GAAP earnings (and therefore can get to cash break-even faster) is not the same thing as saying that only cash flows matter. Because there’s an enormous line item that appears in GAAP earnings but does not show up as a cash expense, which is: Stock-based compensation.

Over the past few years the SaaS investor community (guilty as charged) has started fixating on the free cash flow number rather than the earnings number (here’s an example of Scale VP excluding SBC from their Rule of 40 calc), for myriad reasons both good and bad. but this produces an unfortunate knock-on effect: Remember, what is measured will be gamed. Because the investor community began to tolerate FCF-positive companies with significant EBITDA losses, companies were incentivized to race to cash flow positive while shifting as much compensation as possible to stock-based compensation.

Here’s an example of a major culprit — Twilio. Here’s Twilio’s levered free cash flow (TTM) over the past 5 years.

You can see that since mid-2019 they’ve run the business with positive free cash flows, not bad for a company growing topline between 40% and 60% YoY (passes the Rule of 40 sniff test). But here’s EBITDA (TTM) over that same timeline:

In 2021 Twilio had $226M of unlevered free cash flow yet lost $672m according to GAAP EBITDA. The biggest line-item by far separating the two was $632m (!) of stock-based compensation.

Is this a good or bad business practice for Twilio? Hard for me to say— perhaps this is extremely value-accretive over the long run. I personally know of several Twilio developers who were recently recruited to our portfolio companies who were subsequently lured back to Twilio with enormous 7-figure stock packages. These were very talented employees, so maybe this was the right thing for Twilio to do. (Certainly 2021 was the year of The Great Resignation — scaling companies like Twilio felt they had to offer bigtime stock packages to retain their best people, it was never more difficult to keep them around!)

But there are valuation implications at stake for investors here. Currently Twilio’s EBITDA margins are below negative-20% and their free cash flow margins are at roughly positive-10%. When investors slide into a “free cash flow is what really matters here” mindset, valuations for companies like Twilio go way up (remember: At 40% annual growth, Twilio passes the Rule of 40 with flying colors using the FCF method). But when investors slide back into the “stock is an expense just like cash” headspace, the Twilio stock price gets punished. I posit that this shift in mindset is precisely what’s been happening over the past 6-8 months:

Conclusion

So what happened to cause the Great SaaS Bubble of 2020? I think it was all 3 of these things — elevated growth persistence expectations, very low discount rates, and an excessive focus on cash flows that ignored stock-based dilution — not just separately, by combining together to reinforce each other in a sort of lollapalooza effect.

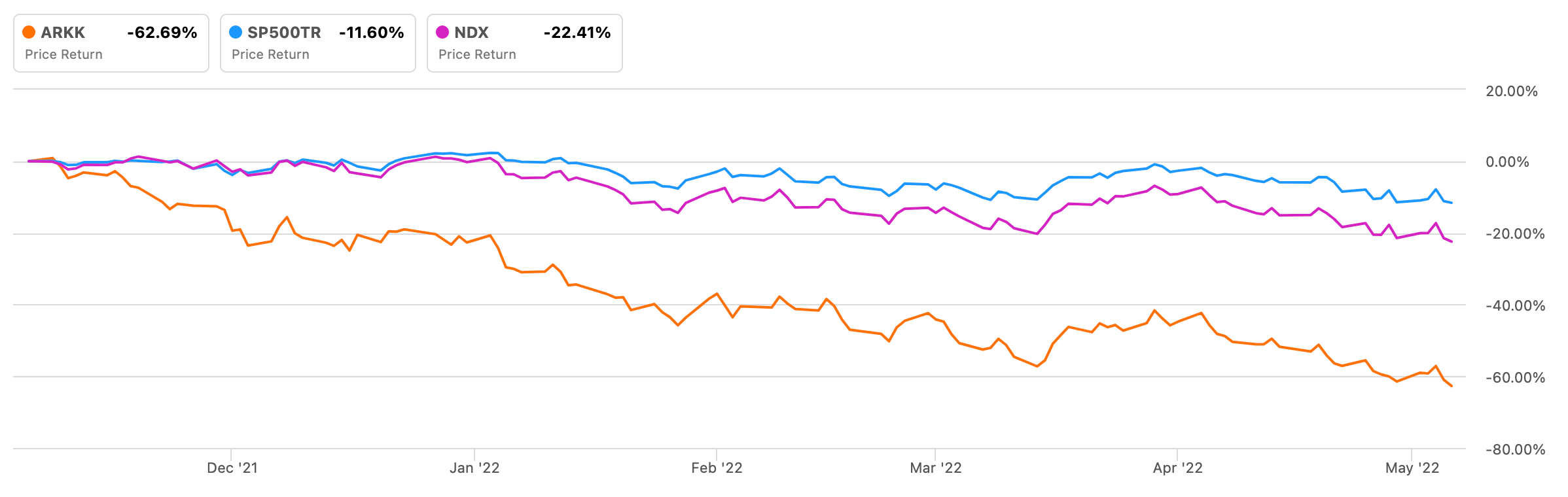

You can verify this by tracing each of these effects back in reverse now that tech equity values are crashing — nobody believes growth persistence will be high in these businesses, especially with looming fears of inflation, war, and recession. Interest rates are rising. The companies farthest from profitability are getting nuked the most. This is why ARKK has been decimated way more than the NASDAQ, because that portfolio is weighted heaviest towards the most speculative businesses — the ones that are growing fast (and therefore most susceptive to variation in growth persistence and discount rates) and are farthest from positive earnings (which frequently end up being the same companies that paid out the most SBC).

So what will happen next? I have no idea. But I at least have a few ideas for how to adapt as an investor.

The biggest thing I’ve decided is that I will no longer allow myself to buy a stock until I build my own DCF model for that business. I bought too many SaaS equities in January and February, thinking I was buying on discount, but not doing the work to determine if they were still overvalued.

Secondly, I’m going to avoid thinking about SaaS companies (to the extent possible) in terms of ARR multiples. The impulse to think that something is “cheap” just because it’s priced at <10x ARR is just too strong. The instrument is too blunt.

Thirdly, a few of these ARKK-type stocks are now on my watchlist. Not to say that a stock is worth buying just because it’s lost 60-80% in value, but rather that it seems likely that some good names are being thrown out with the bathwater. “Watchlist” now means “dedicate a few hours to doing the work”, not “buy when the market opens tomorrow”.

There are a few reasons to be optimistic, and I remain net long the SaaS market in my personal account (in addition to my VC equity which is obviously extremely long the SaaS market). Here are a few of my theses:

I think the market undervalues the hypergrowers with very robust NRR. Whenever I hear somebody say “20 times revenue is too much for ANY company”, I think to myself “this person has probably never really thought hard about how a company like Snowflake works”. A company growing at >80% YoY (at scale) with >150% annual NRR is just a completely different calibre of business than one growing 50% with 130% annual NRR, the mind does not do a very good job of wrapping itself around the steepness of that trajectory. Do with that what you will.

I think that stress is very good for companies. Complacency and arrogance are deadly. Some companies that are spending frivolously will die, but many others will take the hint and cut it out. And become more valuable businesses as a result.

The cloud market is showing no signs of stopping.

Thanks for reading, please let me know what you think.

The sensitivity of valuations to discount rates is important, in part, because of how often the discount rates used are wrong. Like inflation, the discount rate isn't a single number, but for ease of use, is often treated that way. I haven't looked at this, but I bet the heuristics used to compute the discount rate swing with the hype cycle.

Really great perspective through and through!